You are one of the fortunate six million young people who have a Child Trust Fund!

The Child Trust Fund (CTF) is a long-term tax-free savings/investment account for children born in the UK between 1 September 2002 and 2 January 2011. All children within this age range have their own individual account set up under Government arrangements, opened by their parents or HMRC with an initial payment from the Government.

The key purpose of the plan was, and is, to establish a savings habit among children and young people: providing a cushion of financial assets as they embark on adult life, and enabling them to be confident in the management of their finances.

If you were born in the UK between 1st September 2002 and 2nd January 2011, you will almost certainly have a Child Trust Fund. It's a pot of money put into an account for you personally, either via your parents/guardian or directly

What it's worth now depends on three things:

- How much the Government put in: this was typically between £250 and £1,000;

- Whether anyone else put money in, perhaps a member of your family;

- How much it's grown in value over the years.

The money is in an individual account held safely for you with a Child Trust Fund provider.

Most of the accounts were invested in the stock market, and will have grown significantly in value. Some were held as cash deposits and, because interest rates have been so low, these will not have seen so much growth.

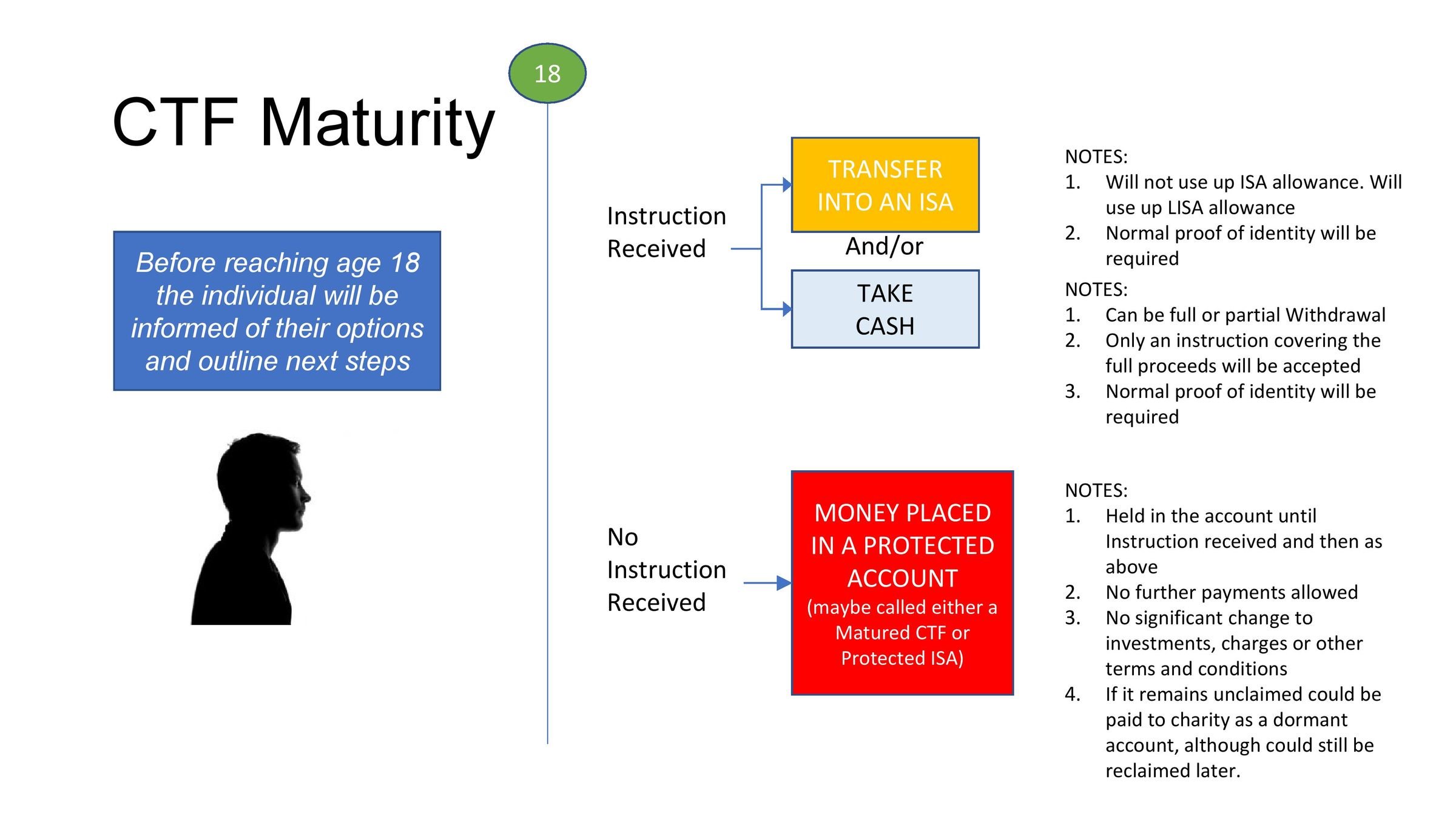

The money is yours and now, from your 16th birthday onwards, you can control the account. The money can be withdrawn when you reach 18, or you can leave it to grow in value.

There's a range of account providers looking after Child Trust Funds safely. As you approach 18, your account provider will need your instructions to tell them what you want to do with your money.

So, to take control of your account, you'll need to contact your account provider and tell them. They'll ask for your contact details and, of course, your identification to check that they're talking to the right person.

Then - make sure you're happy with how it's invested.

For example:

- If you're likely to keep it invested after your 18th birthday it might make sense to leave it in an investment fund, if it's already in one;

- If you're likely to draw the money out at 18, you might prefer to put it in cash now in case market prices fall between now and then;

- Or - you might prefer to learn about investing and choose the investments yourself, in which case you might need to transfer the account to an account provider who offers self selection;

- Or you might prefer to transfer it to a Junior ISA, another type of savings account.

Lots of choices! Welcome to the new world of investing ...

But you do need to make contact - you don't want your money ending up in the red box!

Finally, if you haven't had much financial education at school, now is the time to get more familiar with money: there's a special free eight-week radio course offered by Share Radio in partnership with the Open University which is designed to make it easy to learn about money.

Here's the link to Managing My Money

There's also a web-page with a simple summary for handling your finances, and it's full of links to other resources, including MoneySense.