Managing My Money

Week 7: Pensions and Saving for Retirement - Part 2, Episode 14

Share Radio & Open University Business School

Welcome

to Managing My Money presented by Glen Goodman and Annie Weston

| Known | Unknowns | |

|---|---|---|

| Public Sector | Pension linked to average or final salary | Might raise the retirement date |

| Personal or Workplace Pension | Savings & decisions are in your hands | Subject to swings in the market |

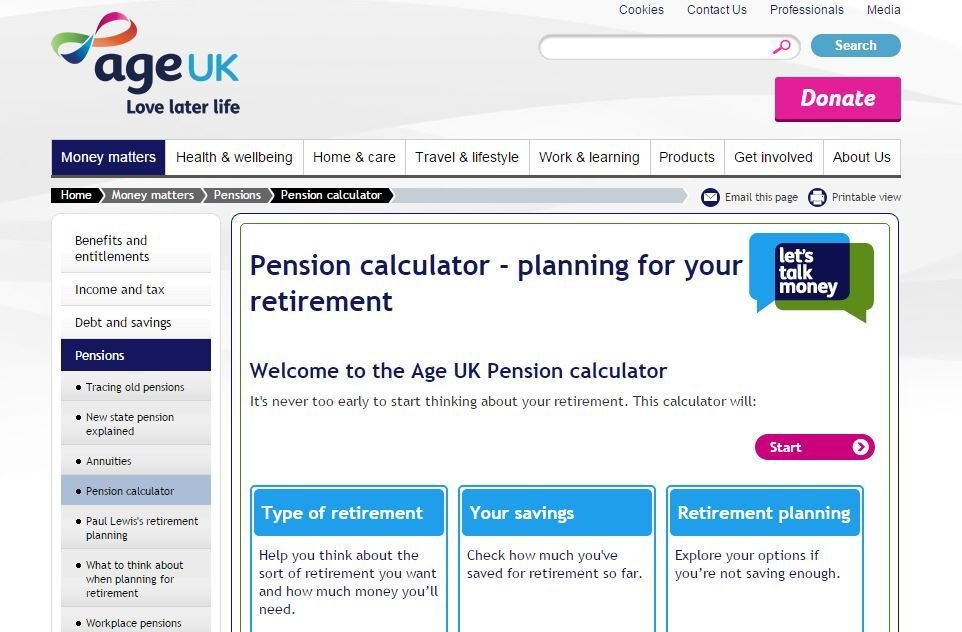

Thinking ahead is vital for planning retirement income

Use the Age UK pension calculator to check your plans ..

The pros and cons of different types of scheme

| Pension type | paid from | Risks |

|---|---|---|

|

Public sector (Defined benefit) |

future taxation | Govt. may move goalposts |

| Private: occupational (Defined benefit) | company reserve from company contributions | Company reserve may go into deficit |

| Private: workplace (Defined contribution) | Automatic enrolment: large pot built from companies, employees & Govt. | Performance uncertain, payout undefined |

|

Private: personal (Defined contribution) |

Personal fund built by your contributions | Performance depends on your decisions, payout undefined |

Tax treatment

The Government's track record for moving the goalposts is not good! But currently -

- Contributions to pensions are made from pre-taxed income

- Investment growth and income within your pension pot are not taxed

- You can take a tax-free lump sum out at retirement

- Retirement income is subject to normal income tax

Things to watch out for

- Fees: over several decades these can make a big dent - so check carefully when you start

- Lost pensions: when people move employment or home, they don't always keep their pension provider informed. Don't lose touch with your money!

- More freedom to access your pension: sounds good, but make sure you won't face a shortfall in retirement

- Annuities: are a way to get steady income post-retirement until you die, but don't give a good return when interest rates are low

- If in doubt, speak to an independent financial adviser!

Do-it-yourself

- Could be the antidote to worrying about fees and what's happening to your pension pot

- Two choices: SIPPs (Self-Invested Personal Pensions) or use ISAs (Individual Savings Accounts)

- You need the time and the aptitude to manage your own investments

ISAs as an alternative to personal pensions

- Contributions are made from your post-tax, not pre-tax, income: but all investment growth (capital gain) and income are tax-free, and your retirement income will not be taxed

- They have been less prone to Government interference

- Annual contribution limit is up to £20,000 (2019/20)

- Access to your money is very flexible - but you must be self-disciplined!

- You can invest in Cash or Stocks & Shares ISAs, either self-invested or using investment funds

Next

Take the Week 7 quiz/test at www.shareradio.co.uk - as you take each week of the course, your results will build up on your personal dashboard.

Managing My Money

is broadcast by Share Radio and is based on the Open University Business School online course of the same name.

Your presenters are Glen Goodman and Annie Weston.