Towards a more egalitarian form of capitalism

Gavin Oldham

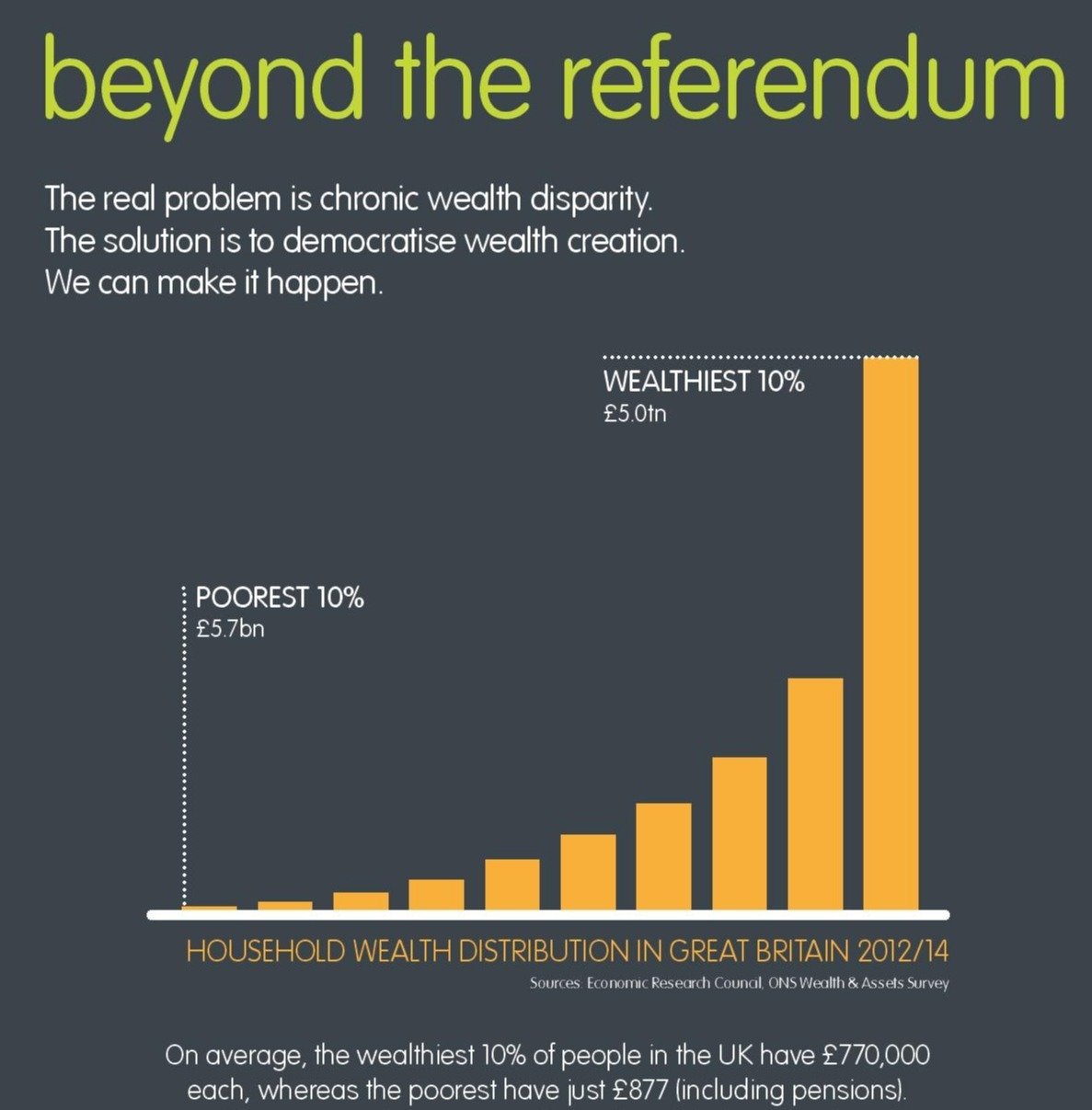

This chart, first published just before the Brexit referendum, shows how polarised wealth in the UK has become. The columns are not cumulative.

Superficially, wealth distribution might seem attractive - but it doesn't work, relying on the politics of envy rather than participation and opportunity. It levels down, not up.

There is no doubt that capitalism and the market economy are at the heart of wealth creation, fostering enterprise and creativity and encouraging the best from people: and yet the rich get richer, the poor poorer and the average age of wealth increases: until something snaps.

Then very large numbers of people with no hope say: “up with this we will not put”, and the pendulum swings once more.

Democratic capitalism not anchored by measures to give genuine equality of opportunity, particularly for the young, is doomed to experience dramatic reverses and to impose a serious degree of unhappiness. This is why this subject is so important.

An egalitarian approach starts with the premise that, as Thomas Jefferson said:

“All are created equal, with unalienable rights to life, liberty and the pursuit of happiness”.

This means that an egalitarian government should not seek to impose solutions on people, but to encourage individual freedom based on equality of opportunity.

In my view, every policy initiative should be tested against these dual yardsticks of individual freedom and equality of opportunity.

Egalitarian Capitalism

Capital Participation for all

Inter-generational rebalancing

The twin pillars of egalitarian capitalism

-

A Treasury task force on capital markets, including:

- a new drive for personal share ownership, in order to reconnect people with business, including encouraging COVID19-based increases in the savings ratio to move into equities, increased voting, and fiscal encouragement for investment clubs recognising their ability to build confidence and knowledge in investment;

- Post-virus re-capitalisation to include direct personal share ownership, incorporating new issue participation and a close look at pre-emption rights - and could this include Government stakes in companies post-COVID19?

- re-balancing the scales between private equity and public markets, to include looking at the treatment of interest, stamp duty, the burden of regulation, and the bias towards business trade sales.

- Form a working group to review whether initiatives to boost home ownership are working, particularly for young people, and the interplay between personal debt and investment;

- Introduce particular focus on tech giants for a new initiative to encourage employee and customer share ownership. These companies could be required to recognise the value of their stored customer data by provision of an equity stake in the business.

Key elements of capital participation for all

Key elements of Intergenerational rebalancing

This is the combination of starter capital accounts and incentivised learning: the latter, so that there is a strong sense of the young person having ‘earned’ the assets.

-

The vehicle for the starter capital accounts would be closely aligned with the Child Trust Fund – it could be a Junior ISA. The Government endowment would only apply to those young people whose families and background leave them without hope of inheritance. The ‘catch up’ for those under 18 who do not currently have a Child Trust Fund would entail a one-off commitment of c. £5 billion but, in the steady state, just a quarter of current inheritance levies targeted at empowering these young people would enable accounts to be established with an initial £1,000, with £1,000 more to follow at age 7.

-

The incentivised learning programme would be introduced to offer the opportunity for them to ‘earn’ a further £3,000 each and, in so doing, prepare themselves to be ready for a fulfilling and economically rewarding adult career. Operated at national level and offered to young people most in need, it would reward those who make the effort to progress through a structured programme of building their life skills with small but meaningful tranches of capital in order to provide a resource base for starting adult life.

Where does the money come from?

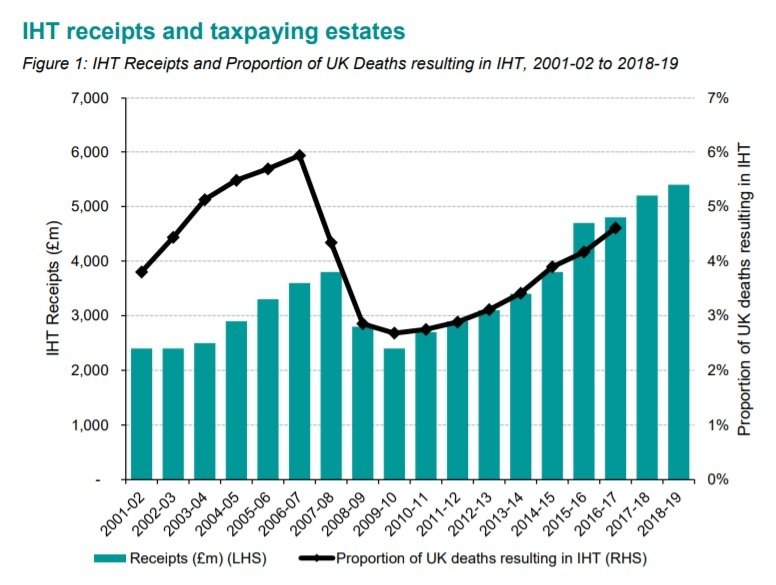

Inheritance Tax is a levy on privately-owned capital which is then placed into the pool to be spent as public expenditure. The process is therefore used to move savings and investment put aside for tomorrow on to the running needs of the present.

It is well known that HM Treasury has an aversion to hypothecation, and of course the proposed financing for inter-generational re-balancing can be drawn from the pool of current spending, but logic suggests that the proceeds of IHT levy, which is paid by under 5% of estates (therefore by those in the wealthiest cohort), at rates set by the Government in power, should at least in some part be employed in financing inter-generational rebalancing.

also - Financial Education

plus - career incentives to reduce or cancel student debt: this would encourage STEM graduates to build a productive career by offering to reduce or write-off their student debt if they remain employed in these occupations for five years post graduation.

The ‘T’ level Finance exam starts in 2021, but subject choices in A levels, essential for university and heavily influenced by university entrance guidelines, do not include financial awareness. Future teachers emerging from universities and teacher training colleges are not equipped to teach the next generation of young people in schools in financial education.

We need a comprehensive and determined approach for improving financial capability:

- A mainstream ‘Financial Awareness’ GCSE, designed to test progress with financial education in schools;

- Guidelines for universities asking schools to bring forward qualifications in life skills and in particular financial capability, and for producing financially capable teachers;

- More focus on primary financial education, where saver/spender attitudes start to develop;

- Proposals to encourage employers in both private and public sectors to provide more adult training in financial awareness. Such training for their staff should be made an allowable expense against gross income.

Forty years ago Sir Keith Joseph spoke of breaking the ‘cycle of deprivation’. A few years before that Martin Luther King said ‘The American dream reminds us that every person is heir to the legacy of worthiness’. Yet little has happened.

Margaret Thatcher tried hard ..

.. but institutional intermediation, privilege and wealth polarisation remain with us today.